HMRC has published updated guidance on the recovery of input tax incurred by holding companies.

The guidance may be found here

It is important for holding companies and/or their advisers to read and understand the changes to the VAT recovery rules as costs are often significant. The changes are a result of various UK and CJEU case law which, in general, considered; the definition of economic activity, the direct and immediate link to taxable supplies made by a holding company, the contractual and payment arrangements and the use of the input tax.

Key Points

The guidance considers:

- When a shareholding is used as part of an economic activity

- Is the Holding Company the recipient of the supply?

- Is the Holding Company undertaking economic activity for VAT purposes?

- Shareholding acquired as a direct, continuous and necessary extension

- Intention to make taxable supplies

- Contingent consideration for management services

- The effect of a holding company joining a VAT Group

- Stewardship costs

- Mixed economic and non-economic activities

Generally

In order to recover the relevant input tax, it must be incurred by a taxable person in the course of an economic activity and have a direct and immediate link to taxable supplies made by that person. This has been a long settled definition and the guidance seeks to apply these tests to holding companies. This means that, in order to receive a supply, a holding company must;

- Contract for it

- Use it

- Be invoiced for it

- Pay for it

Specifically

The publication considers previously disputed situations such as:

- Services provided on contingent terms are not an economic activity because the necessary reciprocity between the obligations of the holding company and of the subsidiary is absent

- How input tax incurred by holding companies which make taxable supplies to some subsidiaries and not to others and those that make taxable supplies and exempt loans should be dealt with

- If a shareholding is acquired as a direct, continuous and necessary extension of a taxable economic activity of the holding company the input tax incurred on acquisition costs may be deducted even if management charges are not made

- A holding company joining a VAT group cannot change a non-economic activity into an economic one or create an automatic link between holding company costs and the taxable outputs of other group members (For VAT to be deductible, the holding company must provide management services to the companies acquired in the VAT group, or earn interest from loans granted to them, and these must support taxable supplies made by the VAT group)

- If a member of a VAT group incurs costs for non-economic (“business”) activity, the supplies are treated as being used by the representative member for non-economic purposes

- Stewardship costs (group audit, legal, brand defence, bid defence etc) are costs for the purposes of the VAT group as a whole rather than for the purposes of the holding company activities

Action

The previous input tax position of holding companies should be reviewed in light of the above guidance and adjustments made as necessary. In some cases, the guidance may provide additional opportunities to reclaim input tax which was previously thought to be barred, and conversely, it is possible that VAT claimed as a result of the understanding of the position at the time may need to be repaid.

We can assist in reviewing the input tax position of holding companies and advising on structures for future intended acquisitions. The four year cap applies to such adjustments of input tax, so the clock is ticking for past transactions.

Image: company stamps

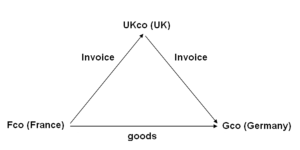

In this example; a UK company (UKco) receives an order from a customer in Germany (Gco). To fulfil the order the UK supplier orders goods from its supplier in France (Fco). The goods are delivered from France to Germany.

In this example; a UK company (UKco) receives an order from a customer in Germany (Gco). To fulfil the order the UK supplier orders goods from its supplier in France (Fco). The goods are delivered from France to Germany.