This case considers the perpetual difficulty of deciding whether activities represent a business… or not.

In the First Tier Tribunal (FTT) case of Healthwatch Hampshire CIC (HH) here the issue was whether HH made taxable supplies by way of business to a Local Authority – Hampshire County Council (HCC)

Background

Under certain prescribed new arrangements, local authorities, including HCC, were required to enter into contractual arrangements with a body corporate, which was required to be a social enterprise and a Community Interest Company (CIC) for the provision of various services.

These services comprised, inter alia:

- Promoting, and supporting, the involvement of local people in the commissioning, provision and scrutiny of local care services

- Information, signposting and advice

- Advocacy services

HH is a company limited by guarantee but is not a charity. It is however non-profit making in its objectives, and any profits which do arise can only be spent for the benefit of the local community. HH was formed by a consortium comprising; three organisations all of which are charities. These charities effectively carried out the work via a sub-contract arrangement and charged HH with the addition of VAT. The issue is the VAT treatment of HH’s charge to HCC. Was this a business activity on which VAT is charged? Or, as HMRC contended, was the money paid to HH was outside the scope of VAT because it represented something which was not consideration for taxable supplies and thus non-business.

This was important as if the services provided by the CIC are deemed to be non-business, the VAT charged to HH by the three consortium members would represent an absolute VAT cost as it could not be VAT registered and therefore not able to recover the input tax.

Technical Note

Because of the special VAT rules which apply to local authorities, input tax incurred by them may be recovered if it relates to their non-business activities (their statutory activities). This is via VAT Act 1994, s33 and this legislation turns “normal” VAT rules on their head. In this particular case, if HH charged HCC VAT, HCC would be in a position to recover it meaning that VAT would be neutral for all parties.

Decision

The matter of whether HH’s activities amounted to a business was considered with significant references to the Longridge On The Thames. Case commentary here

As a starting point, the judge commented on previous CJEU cases that it “…would seem to be a clear demonstration that simply because an activity is normally carried on by the state does not automatically mean that, per se, it cannot be economic activity”. It was also decided that “we have come to the conclusion that HH is not a body governed by public law.” So this strand of HMRC’s argument did not lead anywhere.

The court decided in the taxpayer’s favour; which appears to be common sense all round. The supplies were by way of business despite the arrangements having features which may not necessarily be found in a more commercial environment (including the fact that LAs were legally required to outsource certain of its functions) . Ultimately, consideration was flowing in both directions; HCC paid for supplies which it required and those were supplied by a third party such that VAT was properly chargeable. The fact that HCC met its statutory obligations in structuring transactions in this way did not preclude them being an economic activity.

Action

This case (and Longbridge) demonstrates that where charities, LAs, CICs, NFP entities and similar bodies are concerned, it is crucial to review all agreements from a VAT perspective. It is insufficient to assume the correct VAT treatment is how it is desired and slight differences in arrangements can, and do, produce different VAT outcomes. After Longbridge HMRC are looking more closely at similar arrangements (not limited to LAs) and we expect more of these types of cases to be heard in the future.

For more on the EC aspect of business/non-business please see here

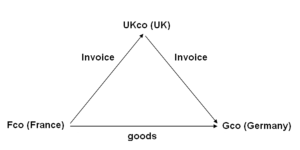

In this example; a UK company (UKco) receives an order from a customer in Germany (Gco). To fulfil the order the UK supplier orders goods from its supplier in France (Fco). The goods are delivered from France to Germany.

In this example; a UK company (UKco) receives an order from a customer in Germany (Gco). To fulfil the order the UK supplier orders goods from its supplier in France (Fco). The goods are delivered from France to Germany.