A new Tribunal case ruled that marshmallows of an unusual size are zero rated, while normal sized marshmallows continue to be standard rated.

A new Tribunal case ruled that marshmallows of an unusual size are zero rated, while normal sized marshmallows continue to be standard rated.

HMRC have announced that the existing Making Tax Digital (MTD) online portal closes on 31 October 2022.

What businesses need to do now (or they could face a penalty)

If businesses haven not signed up to MTD and started using compatible software already, they must follow these steps now:

Step 1

Choose suitable MTD-compatible software they can find a list of software on GOV.UK.

Step 2

Check the permissions in their software – once they have allowed it to work with MTD, they can file their VAT returns easily. Go to GOV.UK and search ‘manage permissions for tax software’ for information on how businesses should do this.

Step 3

Keep digital records for their current and future VAT returns – a business can find out what records they need to keep on GOV.UK.

Step 4

Sign up for MTD and file their future VAT returns using MTD-compatible software – to find out how to do this, go to GOV.UK and search ‘record VAT’.

Businesses who file quarterly or monthly VAT returns must complete these steps in order to file their returns due after 1 November.

Exemption from MTD for VAT

There are exemptions from MTD and they my be applied for here.

HMRC Guidance: Fuel and power (VAT Notice 701/19)

This Notice has recently been updated. It now covers the VAT Reverse Charge measures for wholesale gas and electricity and construction services (Section 2) . There is more information about wholesale gas and electricity and using the VAT domestic Reverse Charge at section 3 of Notice 735: Domestic reverse charge procedure (VAT Notice 735).

Sections 4.1 and 4.3 now include more detail about hydrogen gas.

Brief overview

The reduced rate of VAT of 5% applies to supplies of fuel and power for qualifying use.

Qualifying use means:

Other supplies of fuel and power in the UK are standard rated.

Ferret food has recently been ruled to be subject to 20% tax when previously it was VAT free (from 1973).

Latest from the courts

HMRC has published an update on taxpayers’ appeals. This is a round up of the status of recent cases.

It is helpful for businesses which operate in similar areas, or have tax issues with HMRC and for a general overview on how the courts are approaching certain matters.

The cases which HMRC lose often provide opportunities for retrospective claims for other businesses.

VAT on Staff Expenses – what is claimable?

Although the VAT rules normally prevent a business reclaiming input tax on supplies that are not made directly to it, there are certain circumstances when the rules are relaxed. Although rather a dry and basic area, experience insists that it creates many issues at inspections and is “low hanging fruit” for which HMRC may levy penalties. Some business decide not to recover VAT on such costs to avoid problems, but certain claims are permissible and may be worth significant sums if they have a number of employees.

Subsistence Expenses

For instance, the VAT element of subsistence expenses paid to your employees may be treated as input tax. In order to qualify for this concession, employees must be reimbursed for their actual expenditure and not merely receive round sum allowances. These costs include hotels and meals.

VAT invoices (which may be made out to the employee) must also be obtained. The rule of thumb is that the employee must be more than five miles away from their place of employment and spend over five hours there (the so-called 5 mile/5 hour rule). A business cannot reclaim input tax if it pays an employees a flat rate for expenses.

Reimbursement for Road Fuel

The VAT legislation permits a business to treat as its own supply road fuel which is purchased by a non-taxable person whom it then pay for the actual cost of the fuel (usually through an expenses claim). This would therefore allow a business to recover input tax when it reimburses its employees for the cost of road fuel used in carrying out their employment duties.

A business is able to reclaim all the input tax on fuel if a vehicle is used only for business. There are three ways of claiming VAT if a business uses a vehicle for both business and private purposes.

If a business chooses not to reclaim VAT on fuel for one vehicle it cannot reclaim VAT on any fuel for vehicles used in the business.

Mileage Allowances

The legislation also enables you to reclaim the VAT element (or a reasonable approximation) of mileage allowances paid to employees.

Business entertainment

For details of this complex area please see here

Goods

Certain goods which are to be used in a business, eg; office supplies, the business may reclaim the input tax on purchases made by employees or directors. In all cases you’ll need a VAT invoice. Details required on a VAT invoice here

Mobile telephones

An element of mobile phone costs may be recovered. The VAT on the business use of the phone may be recovered, eg; if half of the mobile phone calls are private 50% of the VAT on the purchase price and the service plan can be recovered.

Work from home

If a person works from home an element of the costs may be recovered. As an example: if an office takes up 20% of the floor space in a house. A business may reclaim 20% of the VAT on utility bills.

Apportionment

A business must keep all records to support a claim and show how it arrived at the business proportion of a purchase of goods or services and it must also have valid VAT invoices.

HMRC has issued new guidance on the amount of input tax claimable when an element is attributable to non-business (NB) activities.

If an entity is involved in both business and NB activities, eg; a charity which provides free advice and also has a shop which sells donated goods, it is unable to recover all of the VAT it incurs. VAT attributable to NB activities is not input tax and cannot be reclaimed. Therefore it is necessary to calculate the quantum of VAT attributable to business and NB activities. That VAT which cannot be attributed is called overhead VAT and must be apportioned between business and NB activities. There are many varied ways of doing this as the VAT legislation does not specify any particular method. Therefore it is important to consider all of the available alternatives. Examples of these are; income, expenditure, time, floorspace, transaction count etc (similar to those methods available for partial exemption calculations).

The new guidance is mainly as a result of the Sveda ECJ case.

The definition of business and NB here.

Legislation: The VAT Act 1994 Section 24(5).

Further reading

The following articles consider case law and other relevant business/NB issues:

Lajvér Meliorációs Nonprofit Kft. and Lajvér Csapadékvízrendezési Nonprofit Kft

VAT – Cross border sales of goods

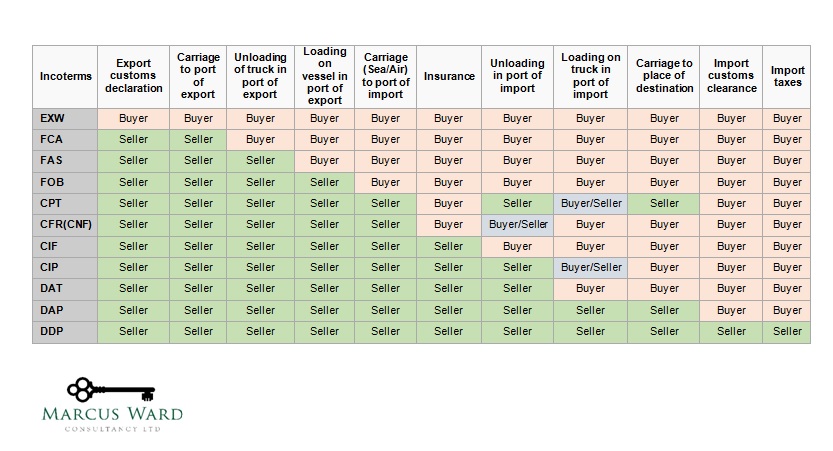

Incoterms stands for International Commercial Terms.

These are published by the International Chamber of Commerce (ICC) and describe agreed commercial terms. These rules set out the responsibilities of buyers and sellers for the supply of goods under a contract. They are very commonly used in cross-border commercial transactions in order that both sides in a transaction are aware of the contractual position. They help businesses avoid costly misunderstandings by clarifying the tasks, costs and risks involved in the delivery of goods from sellers to buyers. The latest terms were published in 2010 and came into effect in 2011.

The use of Incoterms for assistance for VAT purposes

One of the most difficult areas of providing VAT advice is obtaining sufficient detailed information to advise accurately and comprehensively. Quite often advisers are given what a client believes to be the arrangements for a transaction. This may differ from the actual facts, or the understanding of the other party in the transaction.

Pragmatically, this uncertainty about the details may be increased if; a number of different people within an organisation are involved, it is a new or one-off type of transaction, there are language difficulties, or communication and documentation is less than ideal. In such cases, incoterms will provide invaluable information which gives clarity and certainty and usually give a sound basis on which to advise. This enables the adviser to establish the place of supply (POS) and therefore what VAT treatment needs to be applied.

So what is this set of pre-defined international contract terms?

They are 11 pre-defined terms which are subdivided into two categories:

Group 1 – Incoterms that apply to any mode of transport are:

EXW – Ex Works (named place)

The seller makes the goods available at their premises. This term places the maximum obligation on the buyer and minimum obligations on the seller. EXW means that a buyer incurs the risks for bringing the goods to their final destination. The buyer arranges the pickup of the freight from the supplier’s designated ship site, owns the in-transit freight, and is responsible for clearing the goods through Customs. The buyer is also responsible for completing all the export documentation.

Most jurisdictions require companies to provide proof of export for VAT purposes. In an EXW shipment, the buyer is under no obligation to provide such proof, or indeed to even export the goods. It is therefore of utmost importance that these matters are discussed with the buyer before the contract is agreed.

FCA – Free Carrier (named place of delivery)

The seller delivers the goods, cleared for export, at a named place. This can be to a carrier nominated by the buyer, or to another party nominated by the buyer.

It should be noted that the chosen place of delivery has an impact on the obligations of loading and unloading the goods at that place. If delivery occurs at the seller’s premises, the seller is responsible for loading the goods on to the buyer’s carrier. However, if delivery occurs at any other place, the seller is deemed to have delivered the goods once their transport has arrived at the named place; the buyer is responsible for both unloading the goods and loading them onto their own carrier.

CPT – Carriage Paid To (named place of destination)

The seller pays for the carriage of the goods up to the named place of destination. Risk transfers to buyer upon handing goods over to the first carrier at the place of shipment in the country of Export. The Shipper is responsible for origin costs including export clearance and freight costs for carriage to named place (usually a destination port or airport). The shipper is not responsible for delivery to the final destination (generally the buyer’s facilities), or for buying insurance. If the buyer does require the seller to obtain insurance, the Incoterm CIP should be considered.

CIP – Carriage and Insurance Paid to (named place of destination)

This term is broadly similar to the above CPT term, with the exception that the seller is required to obtain insurance for the goods while in transit. CIP requires the seller to insure the goods for 110% of their value.

DAT – Delivered At Terminal (named terminal at port or place of destination)

This term means that the seller covers all the costs of transport (export fees, carriage, unloading from main carrier at destination port and destination port charges) and assumes all risk until destination port or terminal. The terminal can be a Port, Airport, or inland freight interchange. Import duty/VAT/customs costs are to be borne by the buyer.

DAP – Delivered At Place (named place of destination)

The seller is responsible for arranging carriage and for delivering the goods, ready for unloading from the arriving conveyance, at the named place. Duties are not paid by the seller under this term. The seller bears all risks involved in bringing the goods to the named place.

DDP – Delivered Duty Paid (named place of destination)

The seller is responsible for delivering the goods to the named place in the country of the buyer, and pays all costs in bringing the goods to the destination including import duties and VAT. The seller is not responsible for unloading. This term places the maximum obligations on the seller and minimum obligations on the buyer. With the delivery at the named place of destination all the risks and responsibilities are transferred to the buyer and it is considered that the seller has completed his obligations.

Group 2 – Incoterms that apply to sea and inland waterway transport only:

FAS – Free Alongside Ship (named port of shipment)

The seller delivers when the goods are placed alongside the buyer’s vessel at the named port of shipment. This means that the buyer has to bear all costs and risks of loss of or damage to the goods from that moment. The FAS term requires the seller to clear the goods for export. However, if the parties wish the buyer to clear the goods for export, this should be made clear by adding explicit wording to this effect in the contract of sale. This term can be used only for sea or inland waterway transport.

FOB – Free On Board (named port of shipment)

FOB means that the seller pays for delivery of goods to the vessel including loading. The seller must also arrange for export clearance. The buyer pays cost of marine freight transport, insurance, unloading and transport cost from the arrival port to destination. The buyer arranges for the vessel, and the shipper must load the goods onto the named vessel at the named port of shipment. Risk passes from the seller to the buyer when the goods are loaded aboard the vessel.

CFR – Cost and Freight (named port of destination)

The seller pays for the carriage of the goods up to the named port of destination. Risk transfers to buyer when the goods have been loaded on board the ship in the country of export. The shipper is responsible for origin costs including export clearance and freight costs for carriage to named port. The shipper is not responsible for delivery to the final destination from the port (generally the buyer’s facilities), or for buying insurance. CFR should only be used for non-containerised sea freight, for all other modes of transport it should be replaced with CPT.

CIF – Cost, Insurance and Freight (named port of destination)

This term is broadly similar to the above CFR term, with the exception that the seller is required to obtain insurance for the goods while in transit to the named port of destination. CIF requires the seller to insure the goods for 110% of their. CIF should only be used for non-containerised sea freight; for all other modes of transport it should be replaced with CIP.

Allocations of costs to buyer/seller via incoterms

Once the Incoterm has been established, the VAT treatment is usually immediately apparent.

Summary Chart

Latest from the courts

In the Star Services Oxford Limited (Star) First Tier Tribunal (FTT) case the issue was the identity of the entity receiving the supply, whether it held a valid tax invoice, and whether input tax could be claimed.

Background

The appellant claimed input tax incurred on rental payments to Oxford City Council. This was disallowed by HMRC on the grounds that the rental agreement was with Mr Latifi (a sole proprietor in a property rental business) and not the company which was VAT registered.

After the rental agreement was signed the business was incorporated and carried on a bed and breakfast activities from the premises, along with two separate sub-lets to third parties. One party paid rent to Star and one directly to Mr Latifi.

Contentions

HMRC argued that:

Star contended:

Decision

The appeal was dismissed.

The Appellant was not entitled to claim input tax on the invoices and HMRC were correct to disallow input tax. It did not receive the supply and it did not hold a VAT invoice.

It was decided that the legal relationship was between Oxford City Council and Mr Latifi. This is because the lease agreement was between these parties and not the Appellant.

It was found that the rent from one sub-tenant was paid to Mr Latifi directly and is not accounted for by the Appellant and that the reassigned lease has no bearing on the property rental activities undertaken by Mr Latifi prior to the reassignment.

The rules on pre-incorporation supplies* do not apply in this case because Mr Latifi, as sole proprietor, and the Appellant, are separate legal entities, requiring separate VAT registration.

Interestingly, a recent case was relied on: In Tower Bridge GP Ltd the Court of Appeal ruled that absent a valid VAT invoice showing the supplier’s VAT number and the customer’s name, the right to deduct input tax on that invoice could not be exercised.

Summary

An unfortunate oversight was sufficient for HMRC to refuse the input tax claim. This case does have a whiff of unfairness about it, but by applying the letter of the law the outcome is unarguable. The contentions here are similar to those in the Aitmatov Academy case.

Another case of taking care with claims.

* A business may, generally, claim the VAT incurred on services it has purchased for its taxable business purposes during the six months prior to VAT registration .

The VAT Act 1994, s 24(6) (c) and The Value Added Tax Regulations 1995, Reg 111.

You pay VAT on the first 28 days of a stay at a hotel, but from the 29th the accommodation is VAT free.