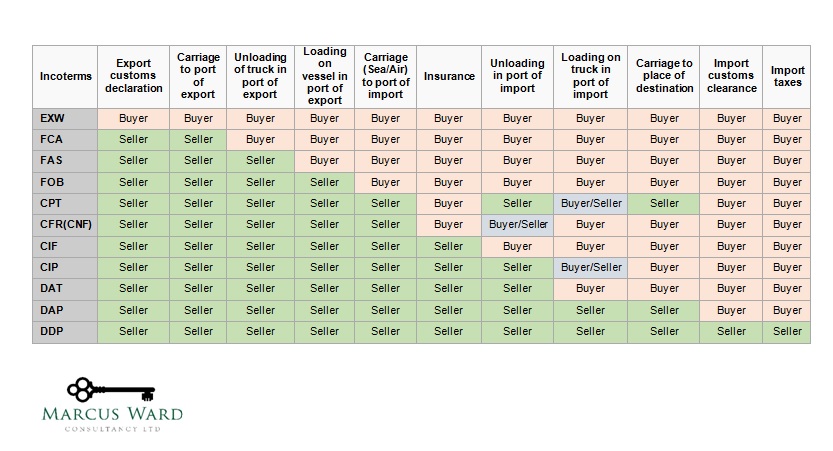

VAT basics

Consignment, call-off stock, and sale or return goods

If a business is required to provide regular sales of goods to customers, a prudent business structure is to keep inventory in a warehouse near the customer, or which belongs to the customer. This is likely to reduce transport costs and provides quicker access to the goods thus reducing time in the supply chain. There are specific VAT rules for businesses which hold stock in foreign countries. They stipulate when, and what VAT should be charged, and if a business needs to VAT register as a non-resident trader in another country in which it is warehousing its goods.

Below we consider what the terms mean, the differences and the VAT treatment applicable.

Differences

There is often confusion over the terms; consignment and call-off stock, and they are sometimes used interchangeably. They are differentiated based on who controls access to, and use of, the goods. The difference determines the VAT requirements and compliance rules, so it is important to identify the actual arrangements a business has in place, or plan for the most beneficial outcome. Both of these measures involve the transfer of a business’ own goods – for the purposes of this article; cross-border. The transfer of goods within the same legal entity from one country to another is a deemed supply. This fact is sometimes missed, which can lead to problems. The VAT rules differ from country to country and create legal uncertainty for businesses.

In summary

- Consignment stock

Consignment stocks are created when a business transfers its own goods to another Member State to create a stock over which it has control and from which it makes supplies. Typically, there are multiple potential customers for consignment stock.

Note: Goods sent to an overseas customer on sale or return are treated in the same way as consignment stocks.

- Call-off stock

Call-off stock is the transfer of goods by a business from one Member State to another to create a stock of goods from which its customers can ‘call-off’ ie; use and pay for the goods as and when they require them.

Not call-off stock

Goods delivered to storage facilities operated by the supplier, rather than the customer, should be treated as consignment stocks (see above). If stocks of goods are dispatched by a supplier for call-off by more than one customer, this is also likely to be consignment stock.

VAT treatment

Consignment stock

There is an initial deemed supply of own goods to form the stock which takes place in the country from which the goods are originally shipped. This is usually VAT free as a dispatch and the usual documentary requirements apply.

The place of subsequent supplies of the goods, once a buyer has been found (change of ownership) is usually the country in which the stock is held.

Because the business is transferring its own goods “to itself” in another country it will be making an acquisition of goods in that country. The business is likely to be liable to register for VAT there (or appoint a fiscal representative in the country of arrival) and be responsible for import obligations in the other country. Output tax will also be due (at the rate of VAT applicable in the country in which the goods are located) on the sale to a third party.

Consignment stock – reporting requirements

If a UK VAT registered business transfers goods to another country to create a consignment stock it must complete box 6 on the VAT return reporting a value based on the cost of the goods – see HMRC Public Notice 725.

Call-off stock

As the customer has control of the goods in storage, is aware of stock movements, and may take stock whenever he requires this does not generally require the seller to VAT register in the foreign country as a non-resident trader. Such sales are treated as a “regular’ export and the seller is required to show the customer’s VAT number etc on invoices and other documentation in order to treat it as VAT free in the usual way. The time of supply for these supplies is the date the goods are called off by the customer.

Call-off stock – reporting requirements

The supply of call-off stock from the UK to a VAT registered business in another country is VAT free (subject to the normal rules). Box 6 of the VAT return should be completed using a value based on the cost of the goods as above.