Latest from the courts

In the First-Tier Tribunal (FTT) case of Procurement International Ltd (PIL) the issue was whether the movement of goods constituted a zero-rated export.

Background

Both parties essentially agreed the facts: The Appellant’s business is that of a reward recognition programme fulfiller. The Appellant had a catalogue of available products, and it maintained a stock of the most ordered items in its warehouse. PIL supplied these goods to customers who run reward recognition programmes on behalf of their customers who, in turn, want to reward to their customers and/or employees (reward recipients – RR). The reward programme operators (RPOs) provide a platform through which those entitled to receive rewards can such rewards. The RPO will then place orders PIL for the goods.

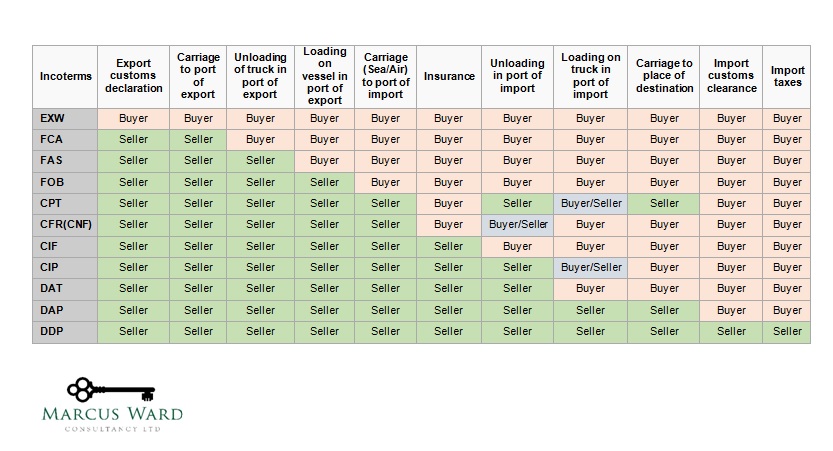

A shipper collected the goods from PIL in the UK and shipped them directly to the RR (wherever located). The shipper provided the services of delivery including relevant customs clearances etc. on behalf of the Appellant. PIL had zero-rated the supply of goods sent to RRs located overseas. All goods delivered to RRs outside the UK are delivered duty paid (DDP) or delivered at place (DAP). As may be seen by Incoterms the Appellant remained at risk in respect of the goods and liable for all carriage costs and is responsible for performing or contracting for the performance of all customs (export and import) obligations. The Appellant was responsible for all fees, duties, tariffs, and taxes. Accordingly, the Appellant is responsible for, and at risk until, the goods are delivered “by placing them at the disposal of the buyer at the agreed point, if any, or at the named place of destination or by procuring that the goods are so delivered”.

Contentions

HMRC argued that in situations where the RPO was UK VAT registered, the appellant was making a supply of goods to the RPO at a time when the goods were physically located in the UK, and consequently there was a standard-rated supply. It issued an assessment to recover the output tax considered to be underdeclared.

PIL contended that there was a supply of delivered goods which were zero-rated when the goods were removed to a location outside the UK. It was responsible (via contracts which were accepted to reflect the reality of the transactions) for arranging the transport of the goods.

Decision

The FTT held that there was a single composite supplies of delivered goods, and these were a zero-rated supply of exported goods by PIL. The supplies were not made on terms that the RPOs collected or arranged for collection of the goods to remove them from the UK. The Tribunal found that the RPOs took title to the goods at the time they were delivered to the RR, and not before such that it was PIL and not the RPOs who was the exporter. This meant that the RPOs would be regarded as making their supplies outside the UK and would be responsible for overseas VAT as the Place Of Supply (POS) would be in the country in which it took title to the goods (but that was not an issue in this case).

The appeal was allowed, and the assessment was withdrawn.

Legislation

Domestic legislation relevant here is The VAT Act 1994:

- Section 6(2) which fixes the time of supply of goods involving removal as the time they are removed

- Section 7 VATA sets out the basis on which the place of supply is determined. Section 7(2) states that: “if the supply of any goods does not involve their removal from or to the United Kingdom they shall be treated as supplied in the United Kingdom if they are in the United Kingdom and otherwise shall be treated as supplied outside the United Kingdom”.

- Section 30(6) VATA provides that a supply of goods is zero-rated where such supply is made in the UK and HMRC are satisfied that the person supplying the goods has exported them

- For completeness, VAT Regulations 1995, regulation 129 provides the framework for the zero-rating goods removed from the UK by and on behalf of the purchaser of the goods.

Some paragraphs of VAT Notice 703 have the force of law which applies here, namely the sections on:

- direct and indirect exports

- conditions which must be met in full for goods to be zero-rated as exports

- definition of an exporter

- the appointment of a freight forwarder or other party to manage the export transactions and declarations on behalf of the supplier of exporter.

- the conditions and time limits for zero rating

- a situation in which there are multiple transactions leading to one movement of goods

Commentary

The Incoterms set out in the relevant contracts were vital in demonstrating the responsibilities of the parties and consequently, who actually exported the goods. It is crucial when analysing the VAT treatment of transactions to recognise each party’s responsibilities, and importantly, when (and therefore where) the change in possession of the goods takes place.