Well, it is nearly Christmas…. and at Christmas tradition dictates that you repeat the same nonsense every year….

Dear Marcus

My business, if that is what it is, has become large enough for me to fear that HMRC might take an interest in my activities. May I explain what I do and then you can write to me with your advice? If you think a face to face meeting would be better, I can be found in most decent sized department stores from mid-September to 24 December.

First of all, I am based in Greenland, but I do bring a stock of goods, mainly toys, to the UK and I distribute them. Where do I belong? Am I making supplies in the UK? Do I pay Customs Duty?

If I do this for philanthropic reasons, am I a charity, and if so, does that mean I do not pay VAT?

I have heard that giving vouchers can be complicated, I think I will need help with these gifts.

The toys are of course mainly for children and I wonder if zero rating might apply? I have heard that small T shirts are zero rated so what about a train set – it is small and intended for children. Does it matter if adults play with it? My friend Rudolph has told me that there is a peculiar rule about gifts. He says that if I give them away regularly or they cost more than £50 I might have to account for output tax. Is that right?

My next question concerns barter transactions. Fathers often leave me a food item such as a mince pie and a drink and there is an unwritten rule that I should then leave something in return. If I’m given Sainsbury’s own brand sherry, I will leave polyester underpants but if I’m left a glass of Glenfiddich I will be more generous and leave best woollen socks. Have I made a supply and what is the value please? My feeling is that the food items are not solicited so VAT might not be due and, in any event; isn’t food zero-rated, or does it count as catering? Oh, and what if the food is hot?

Transport is a big worry for me. Lots of children ask me for a ride on my airborne transport. I suppose I could manage to fit twelve passengers in. Does that mean my services are zero-rated? If I do this free of charge will I need to charge Air Passenger Duty? Does it matter if I stay within the UK, or the EU or the rest of the world? What if I travel to every country? My transport is the equivalent of six horsepower and if I refuel with fodder in the UK will I be liable for fuel scale charges? After dropping the passengers off I suppose I will be accused of using fuel for the private journey back home – is this non-business? Somebody has told me that if I buy hay labelled as animal food I can avoid VAT but if I buy the much cheaper bedding hay I will need to pay tax. Please comment.

May I also ask about VAT registration? I know the limit is £85,000 per annum but do blips count? If I do make supplies at all, I do nothing for 364 days and then, in one day (well, night really) I blast through the limit and then drop back to nil turnover. May I be excused from registration? If I do need to register should I use AnNOEL Accounting? At least I can get only one penalty per annum if I get the sums wrong.

I would like to make a claim for input tax on clothing. I feel that my red clothing not only protects me from the extreme cold, but it is akin to a uniform and should be allowable. These are not clothes that I would choose to wear except for my fairly unusual job. If lady barristers can claim for black skirts, I think I should be able to claim for red dress. And what about my annual haircut? That costs a fortune. I only let my hair grow that long because it is expected of me.

Insurance worries me too. You know that I carry some very expensive goods on my transport. Play Stations, mountain bikes, i-Pads and Accrington Stanley replica shirts for example. My parent company in Greenland takes out insurance there and they make a charge to me. If I am required to register for VAT in England will I need to apply the Reverse Charge? This seems to be a daft idea if I understand it correctly. Does it mean I have to charge myself VAT on something that is not VATable and then claim it back again?

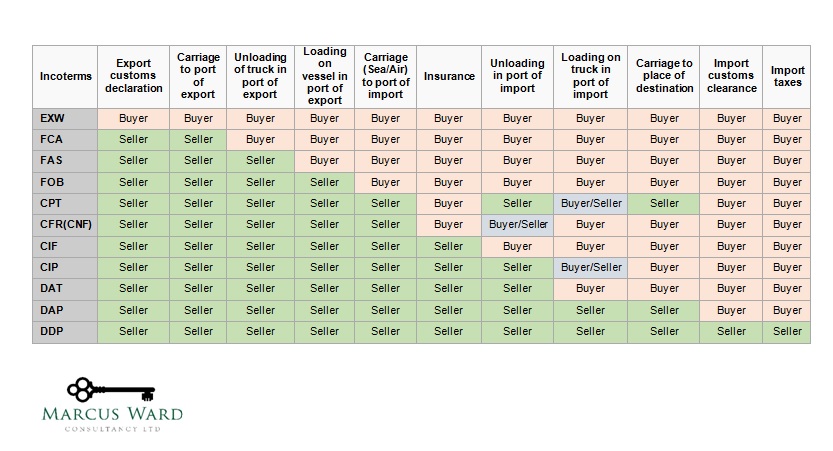

And what about Brexit? I know the UK has already left the EU, but does this affect me? What about distance selling? How do I account for supplies to and from the EU? Will there be Tariffs? Do I have to queue at Dover?

Next, you’ll be telling me that Father Christmas isn’t real……….

HAPPY CHRISTMAS EVERYBODY!